Five Money Numbers to Review Before July

Review five important money numbers before July, including utilities, healthcare, cash reserves, retirement withdrawals and recurring expenses.

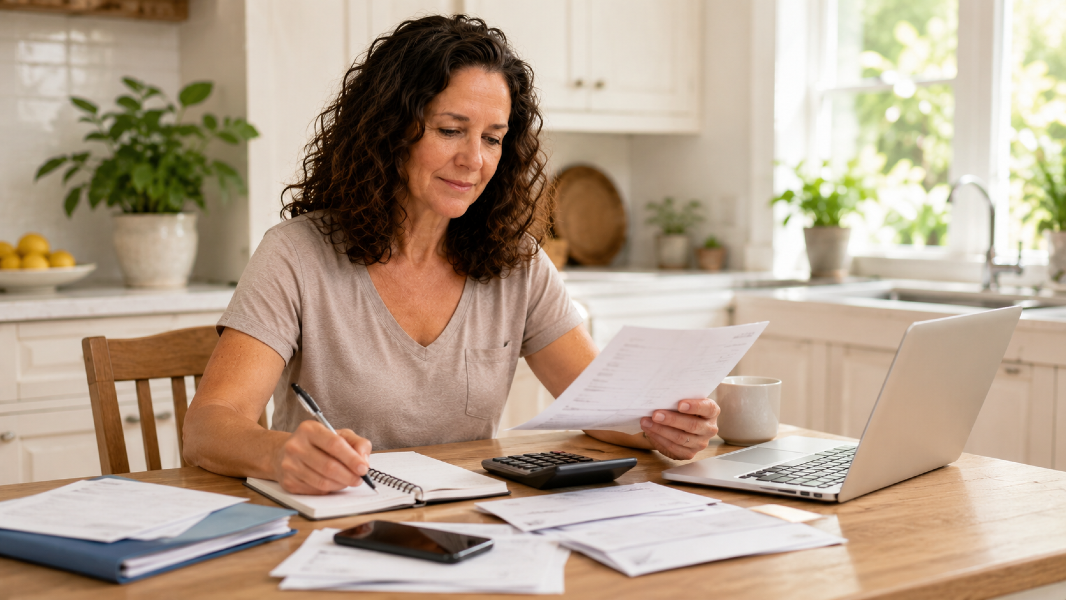

Your Summer Expense Shield: Five Money Numbers to Review Before July

Summer expenses have a way of arriving together.

Electricity increases.

Water use rises.

Travel plans take shape.

Insurance renewals appear.

Home maintenance becomes harder to ignore.

Medical appointments and prescription costs continue.

At the same time, midyear account statements may bring new questions about retirement savings, investment performance and whether the household budget is still working.

You do not need a complicated financial overhaul.

A focused review of five numbers can help you see where pressure is building before it becomes a bigger problem.

Number 1: Your Average Summer Utility Cost

Start with electricity and water.

Look at what you paid during the same months last year.

Then compare that with your most recent bill.

Questions to ask:

How much did electricity increase?

Has water use changed?

Are rates higher, or is usage higher?

Is the air conditioner running longer?

Are there new fees?

Create a realistic summer estimate rather than using the lower amount from spring.

If last July’s electric bill was significantly higher than May’s, use that history to plan for the next two months.

Ways to Reduce Costs Without Sacrificing Safety

Use fans to improve air circulation, but do not rely on fans alone during dangerous heat.

Close blinds during the hottest part of the day.

Check weather stripping around doors and windows.

Replace dirty air filters.

Use major appliances during cooler hours when practical.

Check whether your utility company offers budget billing, senior discounts or limited-income assistance.

Cooling is a health and safety expense, not a luxury during extreme heat. Cost-cutting should never make the home unsafe.

Number 2: Your Monthly Healthcare Out-of-Pocket Total

Healthcare costs are often spread across several places.

Insurance premiums

Prescription copays

Specialist visits

Dental care

Vision care

Over-the-counter products

Medical equipment

Deductibles

Add up the average monthly cost rather than looking at each charge separately.

This gives you a more honest view of how much healthcare is using from the household budget.

Check whether any prescriptions increased.

Review upcoming specialist visits.

Look at whether deductibles or copays have changed.

If a medication cost is becoming difficult, contact the prescribing office, pharmacist or insurance provider to ask about covered alternatives, manufacturer programs or discount options.

Do not stop or change medication without medical guidance.

Number 3: Your Emergency Cash Reserve

Summer can bring heat-related repairs, storm damage, car trouble, medical costs or unexpected travel.

Ask one direct question:

How much money could we access quickly without using a high-interest credit card?

Your emergency reserve does not need to be perfect.

It needs to be visible and intentional.

Review:

Current savings balance

Upcoming known expenses

Insurance deductibles

Car or home repair risks

Travel commitments

Expected medical costs

Even a smaller reserve creates more options than having no buffer at all.

If the reserve is lower than you want, choose one realistic summer contribution amount.

That may be $25, $50 or $100 per paycheck.

The habit matters.

Number 4: Your Retirement Withdrawal Percentage

For anyone drawing from retirement savings, midyear is a useful time to review withdrawals.

Look at:

How much has been withdrawn so far this year

Whether withdrawals increased

Whether the account balance changed significantly

Whether spending is higher than expected

Whether one-time expenses are becoming recurring expenses

Do not make sudden investment decisions based on one market headline.

A retirement account may rise and fall throughout the year.

The more important question is whether the current withdrawal plan still matches your income needs, risk tolerance and long-term goals.

For major changes, speak with a qualified fiduciary financial professional or tax adviser who can review your specific situation.

Number 5: Your Recurring Monthly Commitments

Small monthly charges can become large annual expenses.

Review:

Streaming services

Apps

Cloud storage

Memberships

Subscription boxes

Delivery services

Extended warranties

Phone add-ons

Insurance riders

Automatic donations

Add the monthly charges together.

Then multiply by 12.

A $15 monthly service becomes $180 per year.

Five small subscriptions can easily become $600 to $1,000 annually.

Cancel what you do not use.

Keep what genuinely supports your life.

The goal is not deprivation. It is alignment.

Add a Scam Protection Check

Summer can bring travel scams, utility shutoff threats, storm-repair scams, Medicare impersonation and fake Social Security messages.

Remember:

Government agencies generally do not demand immediate payment through gift cards, cryptocurrency or wire transfers.

Utility companies do not need remote access to your computer.

Do not click unexpected payment links in texts or emails.

Do not give account numbers or verification codes to an unsolicited caller.

Pause before acting.

Contact the organization using a phone number from an official statement, card or website.

Scammers create urgency because urgency reduces judgment.

Your 30-Minute Midyear Money Review

Set a timer for 30 minutes.

Review only these five areas:

Summer utility estimate

Monthly healthcare total

Emergency reserve

Retirement withdrawals

Recurring charges

Write down one action for each.

Examples:

Increase the July utility budget.

Call the pharmacy about a prescription price.

Transfer $50 to savings.

Schedule a retirement review.

Cancel one unused subscription.

That is enough for one session.

Final Thoughts

Financial security is not built through one perfect decision.

It is protected through regular attention.

Summer expenses become easier to manage when you see them coming.

Review the numbers before July.

Adjust the budget before bills arrive.

Question unexpected charges.

Protect your account information.

Ask for qualified help before making major retirement decisions.

A clear picture is more useful than vague worry.

Flex your plant power and keep thriving.

Financial Disclaimer:

This article is for general educational purposes and does not provide individualized financial, investment, tax, legal or insurance advice. Consider consulting an appropriate qualified professional regarding your personal circumstances.

Disclaimer:

This content is for informational purposes only and is not medical advice. Always consult your healthcare provider before making changes to your diet, supplements, or lifestyle, especially if you have existing conditions or take medication.

💌Want plant-based tips each week

Join the Plant Based Flex newsletter. It’s free, and when you confirm your email I’ll send you a 7-Day Kickstart Wellness Bundle to help you thrive beyond 60.